by: Deependra Singh¹

¹Department of Computer Science & Engineering, Chandigarh College of Engineering and Technology (CCET), Chandigarh, India, saharandeependra@gmail.com

Abstract

Most of the transactions of equities currently happening at major stock exchanges are automated. Not only that, but the models behind such transactions are typically difficult for their creators to understand. Complicating matters further is when there are more than one AI agents working in tandem. This paper looks into the use of Multi-Agent Reinforcement Learning combined with Explainable Artificial Intelligence in creating a model for trading which is dynamic and explainable. We will look into the structure of such an approach, starting from the data acquisition phase, agent interactions, to the use of SHAP and LIME to make sense of the process. We present findings that include an accuracy of 85% and F1-score of 0.86 based on market data.

Keywords: Multi-Agent Reinforcement Learning, Explainable AI, Algorithmic Trading, Fintech, Deep Reinforcement Learning, Financial Decision Systems

Introduction

From 60 to 75% of trades on major stock exchanges are carried out by automatic systems today; an increasing number of these automatic systems are based on deep learning algorithms rather than rule-based approaches [1,2]. Such a development has led to a situation that regulators from both sides of the Atlantic cannot tolerate anymore – when a model based on millions of market situations decides to make a trade, it becomes extremely difficult to understand how this happened even for the organization owning it [2,3]. Even more complicated the situation is when there are multiple AI-driven participants, such as market makers, trend followers, and arbitrageurs, working at the same time, which leads to emergence effects that were not intended in any single model [2,3]. In this regard, the combination of MARL and XAI looks like an effective solution, as MARL solves one side of the problem while XAI the other.

Foundations of Multi-Agent Reinforcement Learning in Fintech

In conventional reinforcement learning, an individual agent learns its policy π(a|s) from interaction with the environment, which is presumed to remain constant as the agent becomes better at it. Deep Q-Networks (DQN), Proximal Policy Optimisation (PPO), actor-critic and other commonly-used approaches operate on precisely this presumption. For applications involving financial markets, this can be dismissed straight away. In MARL, there is no such presumption. It posits N agents learning policies in parallel, and the action taken by each of them affects the state observed by agent i. The canonical algorithms of MARL—MADDPG, QMIX and MAPPO—approach the joint action space in their own way. But all of them feature one common property: the reward earned by agent i relies on the policy of agent j [2]. And SARIN et al. have found out that trading roles correspond well to that model.

The Q-learning update,

Qₜ₊₁(s,a) = (1 − α)·Qₜ(s,a) + α·[r + γ·maxₐ′ Qₜ(s′,a′)]

is extended in MARL with coupled reward functions, explicitly representing the adversarial–cooperative duality of real markets.

Integrating Explainable AI into the MARL Pipeline

A decision that can be explained only by making sense of the strategy being developed by another agent is genuinely difficult to explain. This problem has two kinds of solution approaches: intrinsic techniques (attention-based policy heads, symbolic distillation) and post-hoc techniques (SHAP, LIME, counterfactuals) [4]. The SHAP technique uses Shapley values from cooperative game theory and measures:

φᵢ = Σ_{S⊆F∖{i}} [|S|!(p−|S|−1)!/p!] · [f(S∪{i}) − f(S)]

This is precisely what financial analysts require: an ethical rationale for the decision to weigh order-book imbalance over implied volatility for a specific transaction [1,4]. LIME serves as an extension of SHAP, in which local surrogate models are built around each decision. The new way of explaining actions uses explanation regularization that penalizes a policy for any sudden change in Shapley attributions when transitioning from one state to another in the training process [5].

Operational Pipeline and Empirical Evidence

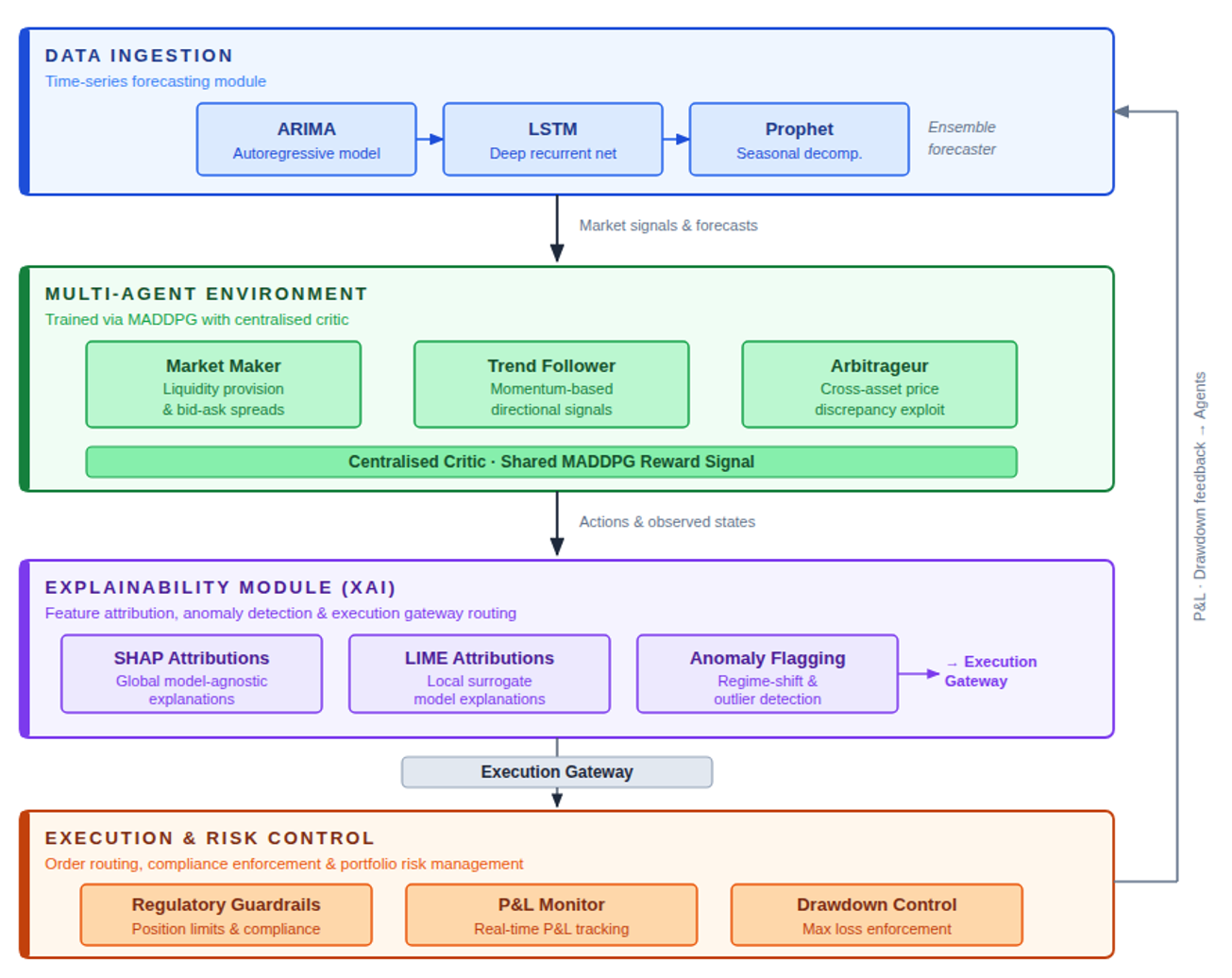

The MARL+XAI system deployed in production is made up of four layers, which is represented in Figure 1. The data layer uses tick-by-tick order book, macroeconomic factors, and news sentiment data. The model employed in the forecasting task by this layer is a combination of ARIMA, LSTM and Prophet models with an accuracy rate of 93% for related tasks [6]. The agent layer consists of market makers, trend followers, and arbitrage agents that are developed through MADDPG in the CTDE (centralized training and decentralized execution) framework. This framework entails that while each agent acts based on its own observation during testing, there is centralized critic during training. The XAI layer provides SHAP and LIME interpretation, flags any unusual decision to the execution gateway, and returns interpretability score to train the agents [1,7].

In Sarin et al.’s comparison between MARL+XAI model named “NeuroAlpha Vintage Explorer” with the baseline models like MACD and Random Forest on the “Alpha Vintage” dataset, the performance metrics are found to be Accuracy = 0.85, Precision = 0.88, and F1-score = 0.86 [1]. The transparency methods do not seem to sacrifice performance.

Challenges and Ethical Considerations

This doesn’t mean that the framework is complete. The core challenge is non-stationarity. The standard guarantees in reinforcement learning require a stationary environment; however, the fact that all agents optimize their policies at the same time makes these guarantees invalid. The vulnerability to adversarial behavior emerges right from the fact of transparency, inasmuch as once the agent realizes how the MARL system gives weight to the order imbalance, she can easily use spoofing orders to skew the rewards. Not only can increasing interpretability make the system vulnerable to attack, but it could be further exacerbated by the fact of accuracy-interpretability conflict. SHAP values for correlated features tend to fluctuate [1,4].

Indeed, the ethical issues are just as serious. Historical market bias embedded in training data creates biased agents, which put small investors at a disadvantage [8]. Federated learning with homomorphic encryption helps in some ways, making it possible for companies to jointly train agents without revealing their proprietary order flows [5]; yet it has problems of its own. In large numbers, MARL agents can exhibit flash-crash dynamics that none of the companies anticipated and that circuit breakers never accounted for.

Open Research Issues and Future Scope

Some promising avenues need exploration. The application of quantum computing to reinforcement learning may reduce training times of policies from days to hours and facilitate retraining as market regimes change. Cross-market federated MARL, where agents at different financial institutions communicate gradient information without sharing trade information, has not yet been explored; the challenge here is progress in the field of homomorphic encryption and verifiable computing [5]. Standards for regulatory XAI have to be formulated; currently, there is no set of criteria for what would constitute an adequate explanation. Also, there is the matter of the direction that MARL should take; while equity markets are unique, decentralized finance, carbon markets, and auctions for sovereign debt have entirely different microstructure and participants.

Conclusion

The marriage of MARL and XAI provides strong evidence that, contrary to widespread beliefs, adaptiveness of performance does not have to come at the cost of transparency and explainability. This has been supported empirically by the application of the MARL-XAI approach to benchmark datasets; additionally, integrating Shapley contributions to the learning process as opposed to considering them as an afterthought is a significant methodological advancement [1]. However, there will be many hard issues that will need to be solved beyond improvements in the model architecture – such as adversarial robustness, training instabilities, biases embedded in legacy data, and risks posed by agent correlations. These cannot be addressed without exercising judgement on how and when to deploy ML.

References

- S. Sarin, S. K. Singh, S. Kumar, S. Goyal, B. B. Gupta, W. Alhalabi, and V. Arya, “Unleashing the Power of Multi-Agent Reinforcement Learning for Algorithmic Trading in the Digital Financial Frontier and Enterprise Information Systems,” Computers, Materials & Continua, vol. 80, no. 2, pp. 3123–3138, 2024. doi: 10.32604/cmc.2024.051599.

- A. Shavandi and M. Khedmati, “A multi-agent deep reinforcement learning framework for algorithmic trading in financial markets,” Expert Systems with Applications, vol. 208, p. 118124, 2022. doi: 10.1016/j.eswa.2022.118124.

- Y. Huang, C. Zhou, K. Cui, and X. Lu, “A multi-agent reinforcement learning framework for optimizing financial trading strategies based on TimesNet,” Expert Systems with Applications, vol. 237, p. 121502, 2024. doi: 10.1016/j.eswa.2023.121502.

- A. B. Arrieta et al., “Explainable Artificial Intelligence (XAI): Concepts, taxonomies, opportunities and challenges toward responsible AI,” Information Fusion, vol. 58, pp. 82–115, 2020. doi: 10.1016/j.inffus.2019.12.012.

- B. B. Gupta, A. Gaurav, and V. Arya, “Secure and privacy-preserving decentralized federated learning for personalized recommendations in consumer electronics using blockchain and homomorphic encryption,” IEEE Transactions on Consumer Electronics, vol. 70, no. 1, pp. 2546–2556, 2024. doi: 10.1109/TCE.2023.3342139.

- S. Kumar, S. K. Singh, H. Singh, V. Arya, and B. B. Gupta, “Advanced Web Traffic Modelling and Forecasting with a Hybrid Predictive Approach,” Journal of Web Engineering, 2024. [Verify volume/issue/pages at River Publishers before submission.]

- G. Mengi, S. K. Singh, S. Kumar, D. Mahto, and A. Sharma, “Automated Machine Learning (AutoML): The Future of Computational Intelligence,” in International Conference on Cyber Security, Privacy & Networking, Bangkok, Thailand. Cham: Springer International Publishing, 2021, pp. 309–317.

- S. M. Lundberg and S.-I. Lee, “A Unified Approach to Interpreting Model Predictions,” in Advances in Neural Information Processing Systems 30 (NIPS 2017), Long Beach, CA, USA, 2017, pp. 4765–4774.

- Elechi, P., Ekolama, S. M., Okowa, E., & Kukuchuku, S. (2025). A review of emerging technologies in wireless communication systems. Innovation and Emerging Technologies, 12, 2550005.

Cite As

Sing D. (2026) Explainable Multi-Agent Reinforcement Learning for Algorithmic Trading, Insights2Techinfo, pp.1